-

Understanding primary immunodeficiency (PI)

Understanding PI

The more you understand about primary immunodeficiency (PI), the better you can manage it. Learn about PI diagnoses and treatment options.

-

Living with PI

Living with PI

Living with primary immunodeficiency (PI) can be challenging, but you’re not alone—many people with PI lead full and active lives. With the right support and resources, you can, too.

-

Get involved

Get involved

Be a hero for those with PI. Change lives by promoting primary immunodeficiency (PI) awareness and taking action in your community through advocacy, donating, volunteering, or fundraising.

-

Advancing research and clinical care

Advancing research and clinical care

Whether you’re a clinician, researcher, or an individual with primary immunodeficiency (PI), IDF has resources to help you advance the field. Get details on surveys, grants, and clinical trials.

Key points:

- Know your family’s medical needs and past use of health plan benefits before choosing a healthcare plan.

- Compare benefits, drug formulary lists, and provider networks (if applicable) across several plans to help determine which one offers the best balance of price versus coverage for you.

- Choose you Medicare options carefully, especially if you are on immunoglobulin replacement therapy.

How to choose an insurance plan

When it comes to health insurance, you need to be your own advocate—and that starts with asking questions. It’s your responsibility to understand your plan, no matter how you and your family get coverage. You’ll want to find a plan that’s right for you because it can have a huge impact on your health and finances.

Choosing the right health insurance plan can be a daunting task. It’s crucial to understand your plan's details and make an informed decision to ensure both your health and finances are protected. Always review a plan's summary of benefits, drug formulary list, and provider network directory.

Questions to ask before deciding on a health plan:

- What is the premium?

- What is the out-of-pocket maximum?

- What are the deductibles?

- Is the deductible included in the out-of-pocket maximum, or is it in addition to the maximum?

- How is immunoglobulin (Ig) therapy covered?

- Do you have coinsurance or a flat copay for treatments and services you are likely to need?

- Do you have options for the site of care?

- Are your physicians in the plan's network?

- Are there out-of-network benefits?

- Does the plan have a copay accumulator?

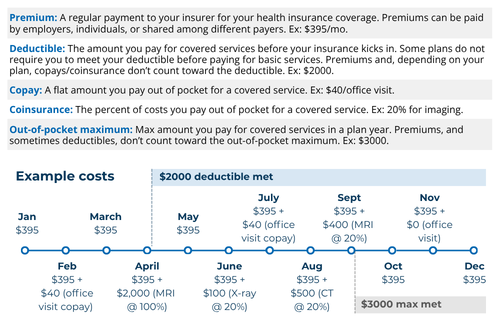

Here are definitions for common health insurance terms. An example health insurance plan might have a premium of $395/month, a $2000 deductible, a $40 copay for office visits, 20% coinsurance for imaging tests, and a $3000 out-of-pocket maximum. The timeline shows a person's out-of-pocket costs and how each item applies for each month during the year with the example plan.

Medicaid eligibility and enrollment

You may qualify for free or low-cost healthcare through Medicaid based on income and family size. Eligibility rules vary from state to state. In all states, Medicaid provides health coverage to some children, parents, pregnant women, elderly people with certain incomes, and people with disabilities. Some states have expanded their Medicaid programs to cover other adults below a certain income.

There are two ways you can apply for Medicaid:

- Directly with your state at your local county job and family service office.

- Through the health insurance marketplace.

Filing appeals and complaints

If your insurer denies a claim, you have the right to appeal. You can also consider filing a complaint.

This page contains general medical and/or legal information that cannot be applied safely to any individual case. Medical and/or legal knowledge and practice can change rapidly. Therefore, this page should not be used as a substitute for professional medical and/or legal advice. Additionally, links to other resources and websites are shared for informational purposes only and should not be considered an endorsement by the Immune Deficiency Foundation.

Adapted from the IDF Patient & Family Handbook for Primary Immunodeficiency Diseases, Sixth Edition.

Copyright ©2019 by Immune Deficiency Foundation, USA

Sign up for updates from IDF

Receive news and helpful resources to your cell phone or inbox. You can change or cancel your subscription at any time.